Where serious crypto decisions get made.

Macro tells you if and when to be exposed — live macro, cycle, on-chain, and execution inputs synthesized into one verdict. Desk turns that verdict into pre-trade thesis context. One engine for the allocation decision, with accountability attached.

00Start here

One Bitcoin state, five decision views. Start with the verdict; open only evidence that can change it.

| Destination | Question it answers | Route |

|---|---|---|

| Bitcoin State | What is Bitcoin's complete state right now? | /state |

| Today's Read | What are the five decisions now? | /macro |

| Desk | What evidence and invalidation govern execution? | /desk |

| Track Record + Ledger | How has the system performed, and can I verify the record? | /track-record · /ledger |

| AI Agents | How can software use the same synthesis? | /agents |

| Site Map | Where does every active page live? | /sitemap |

State → decision → evidence → action → accountability. Bitcoin State holds the complete thesis. Now, Cycle, Money, Macro, and Action keep each decision concise. Track Record and Ledger preserve the receipts.

00bEvery panel: what it means and how to read it

This is the user field guide for all 31 active Macro panels. Open a panel below for a real interface snapshot, the metric definition, the interpretation rule, the decision it feeds, and the condition that makes the read unsafe.

A synthesis is not a new raw metric. It combines several owned inputs under declared rules. Always read it in this order: verdict → score or state → coverage → agreement → freshness → invalidation. A strong-looking verdict with weak coverage or stale evidence is a weak read.

CryptoWatch compresses eight evidence families into the existing five decisions: entity accumulation, supply liquidity, network demand, holder spending, old-coin activity, miner health, buyer/seller alignment, and ownership-cost position. Confidence is decomposed into coverage, agreement, persistence, historical reliability, and regime relevance. Historical reliability stays unavailable until enough daily receipts exist; the ownership-cost read uses verified cost-basis levels and does not claim to be a full URPD histogram.

Snapshots explain layout and labels; they are not live recommendations. Values can be loading, unavailable, or different from today. Open Today’s Read for the current state.

Now · conclusion and confidence

Smart AlertsFeeds · Bitcoin Now

Threshold crossings in load-bearing cycle, flow, macro, and positioning inputs, with severity, confidence, analog, and base-rate context.

Hard alerts deserve review now. Watch cards are context only. Read severity, driver contribution, then the suggested next check.

A live input crosses its declared threshold and supporting evidence confirms the move.

The card is watch-only, has no base-rate context, or its source is stale.

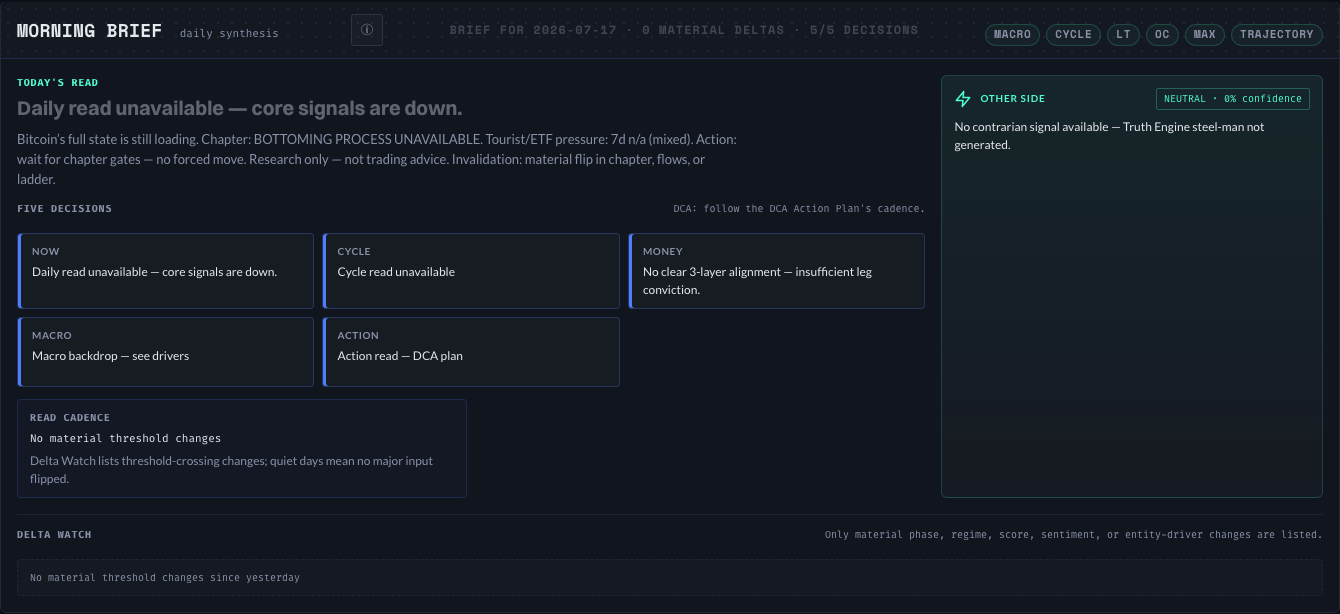

Morning BriefFeeds · Bitcoin Now

The daily synthesis: headline, five decisions, material changes, strongest opposing case, and invalidation.

Start here each day. A quiet Delta Watch means no threshold crossed; it does not mean the data failed to refresh.

A decision or material driver differs from the previous daily brief.

The brief date and underlying snapshot are not current.

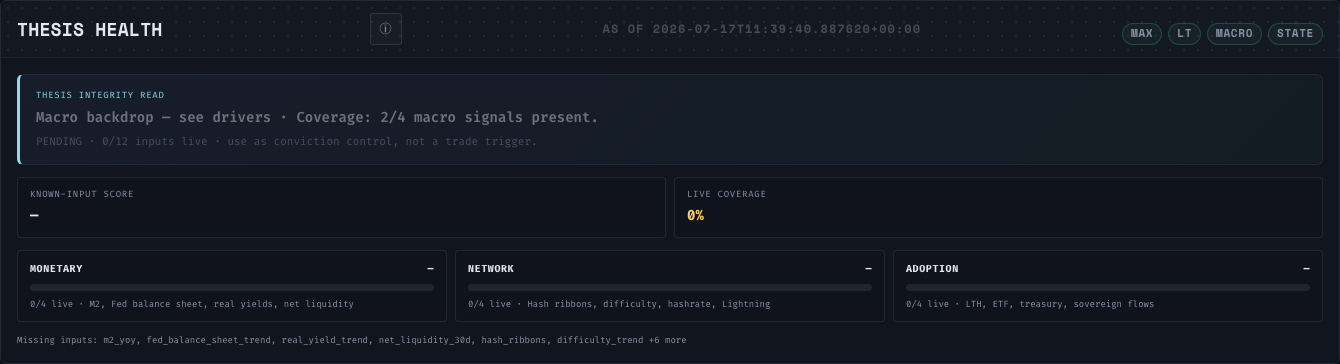

Thesis HealthFeeds · Bitcoin State

Whether monetary liquidity, network strength, and adoption or ownership flows still support the long-term Bitcoin thesis.

Read the known-input score together with live coverage. Strengthening supports conviction; weakening asks for confirmation, not an automatic sale.

One or more thesis pillars weaken enough to change the aggregate state.

Coverage is too low for the displayed confidence.

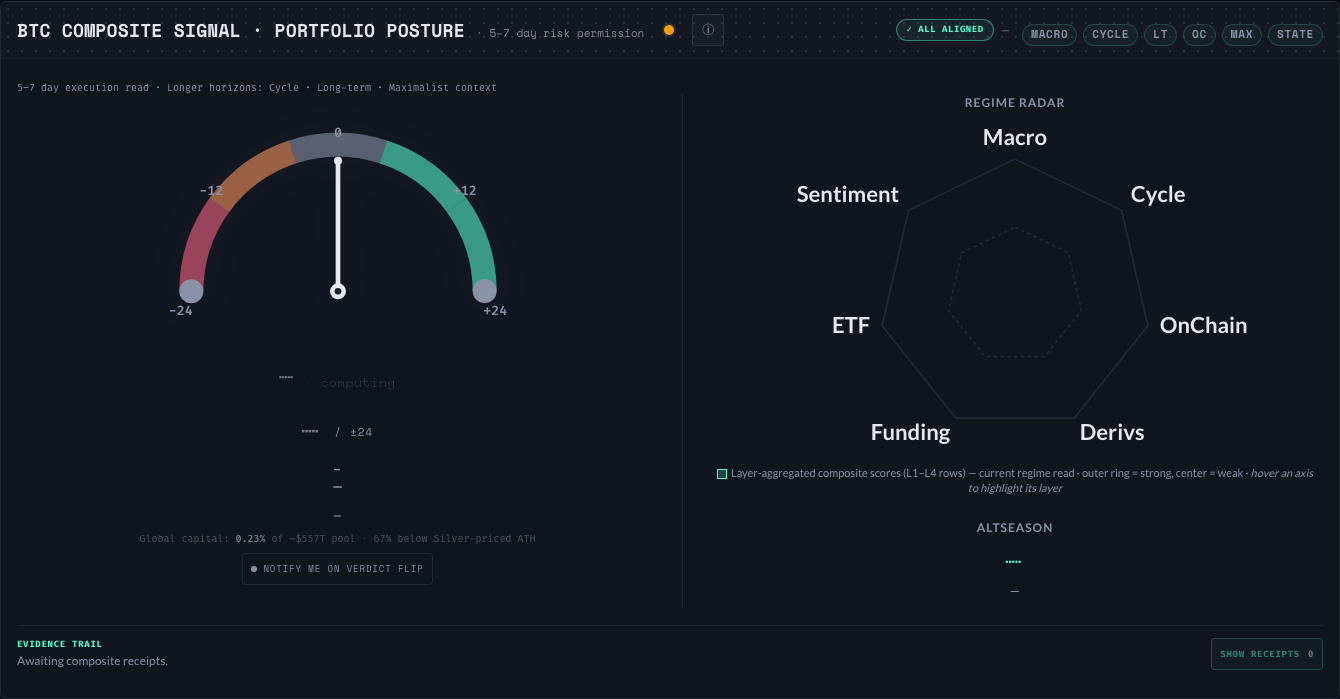

BTC Composite SignalFeeds · Bitcoin Now

A signed −24 to +24 synthesis across Macro, Cycle, On-Chain, and Execution. Each eligible input contributes −2 to +2 before conflict rules and coverage gates.

Negative is defensive, near zero is Wait, positive permits more risk. The gauge is the headline; the radar explains which layers create that result.

The score crosses a verdict band or a binding conflict rule limits the raw score.

Coverage, agreement, freshness, or the evidence trail does not support the posture.

Market CompassFeeds · Macro

Seven regime lenses: macro, cycle, on-chain, derivatives, funding, ETF flows, and sentiment.

Use the shape to see alignment and divergence. A broad outer shape means stronger conditions; a collapsed or lopsided shape means weak or conflicted conditions.

The balance of lenses shifts the market between risk-off, transition, and risk-on states.

Too few lenses are live or one stale lens dominates the map.

Truth EngineFeeds · confidence

Source coverage, agreement, conflicts, and freshness across the evidence used by the main read.

High coverage plus high agreement permits more trust. Low coverage or active conflicts should reduce position size and confidence.

The evidence quality changes the permission to trust the Composite verdict.

You treat it as a separate buy/sell signal. It is a confidence brake.

Cycle · phase, temperature, and extremes

CW Risk ScoreFeeds · Cycle

A normalized 0–1 cycle-temperature score. Values near 0 represent capitulation-like valuation; values near 1 represent euphoria-like valuation.

Cold favors patient accumulation context; hot raises distribution risk. Mid-range values are not actionable without trend and cycle phase.

The score enters a new risk band and its companion signals agree.

Used as an exact top/bottom timer by itself.

Cowen Cycle SuiteFeeds · Cycle

Seven complementary cycle reads covering time, valuation, trend, dominance, and risk.

Count directional agreement, then inspect dissenters. Four or more aligned reads create context; one clock never defines the cycle.

At least four live reads align in one direction.

Fewer than four reads are available or the bundle is older than 26 hours.

Cycle Top RadarFeeds · Cycle

Proximity of MVRV-Z, Puell, Mayer, and related overheating inputs to historically elevated bands.

Low means far from a confirmed top cluster. Elevated means several measures are stretched. It estimates proximity, not a date.

The proximity score enters Elevated or Risk and distribution evidence agrees.

Fewer than two core valuation inputs are live.

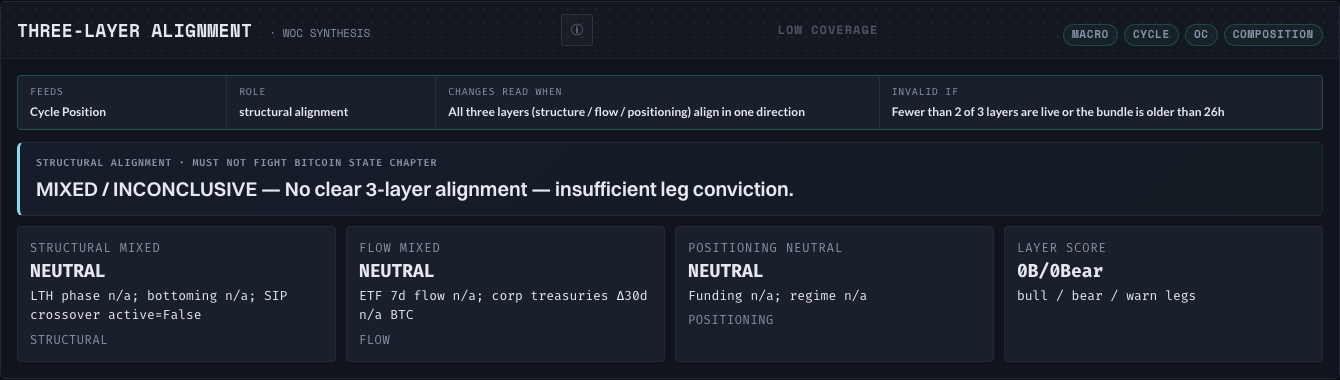

Three-Layer AlignmentFeeds · Cycle

Whether structure, capital flow, and derivatives positioning tell the same directional story.

All aligned raises conviction. Two versus one is partial confirmation. Mixed means wait for the dissenting layer to resolve.

All three layers align or a previously aligned state breaks.

Fewer than two layers are live or the bundle is stale.

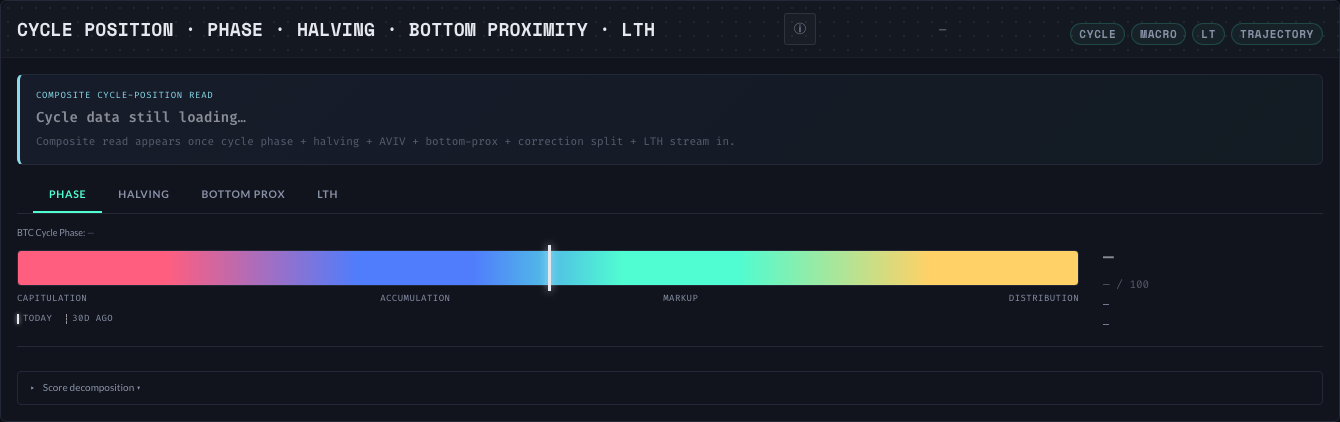

Cycle PositionFeeds · Cycle

A 0–100 phase synthesis combining valuation, halving context, bottom proximity, correction structure, and long-term-holder behavior.

Use the phase label first, then open Phase, Halving, Bottom Proximity, and LTH tabs to see what supports or contradicts it.

The component stack moves the phase into capitulation, accumulation, markup, or distribution.

Calendar phase overrides contradictory live evidence or too few components are available.

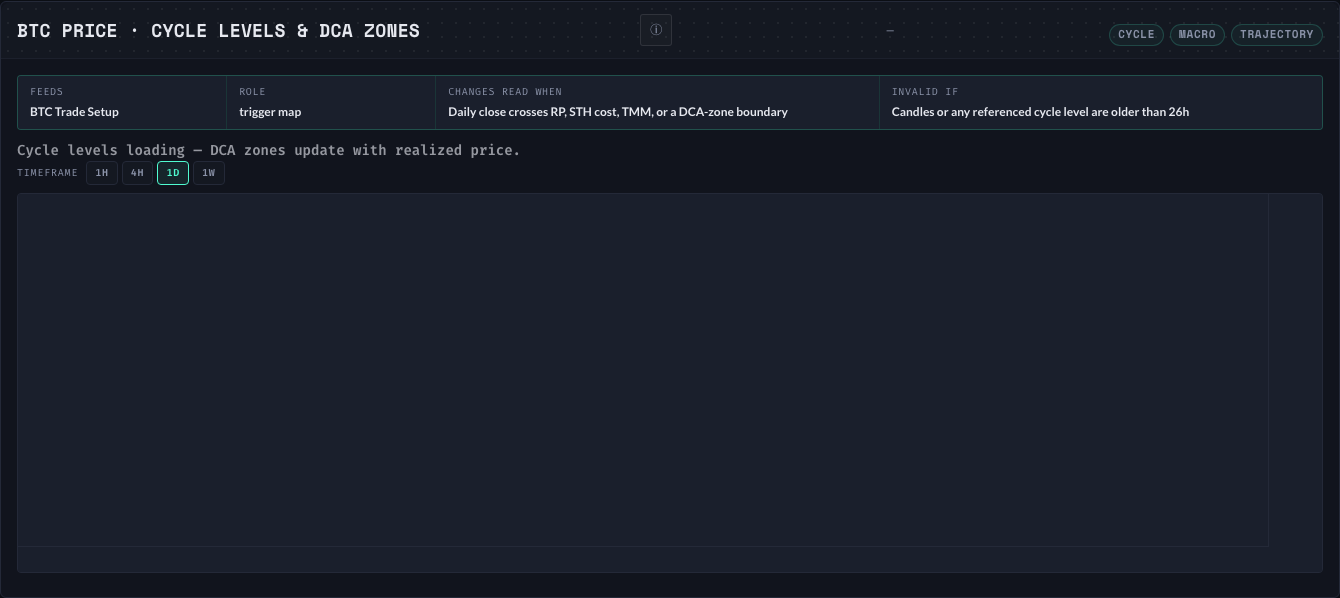

BTC Price · Cycle LevelsFeeds · Cycle and Action

Spot price relative to Realized Price, LTH Realized Price, STH Cost Basis, True Market Mean, and DCA zones.

These are cohort cost and valuation anchors. Reclaiming a level can improve structure; losing it can turn that same level into resistance.

A daily close crosses a referenced level or allocation zone.

Candles or the referenced levels are older than 26 hours.

Money · who is buying and selling

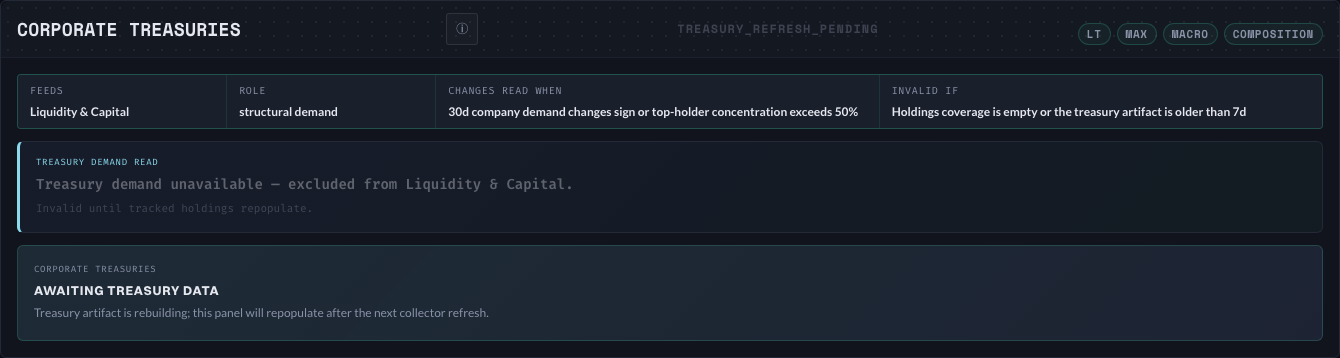

Corporate TreasuriesFeeds · Money

Known company, miner, ETF, and government Bitcoin holdings plus concentration and 30-day demand change.

Rising holdings support structural demand. Concentration above 50% increases entity-specific risk even if total holdings rise.

Thirty-day demand changes sign or concentration crosses its risk threshold.

The holdings artifact is empty or older than seven days.

LTH → Exchange TransfersFeeds · Money

Seven-day average transfer volume from long-term holders to exchanges, split between coins moved in profit and at a loss.

Rising profit transfers suggest distribution. Rising loss transfers suggest stress or capitulation. Transfers are intent evidence, not proof of sale.

Loss transfers exceed 60% while total transfers rise, or sustained profit transfers accelerate.

The split or total moving average is unavailable.

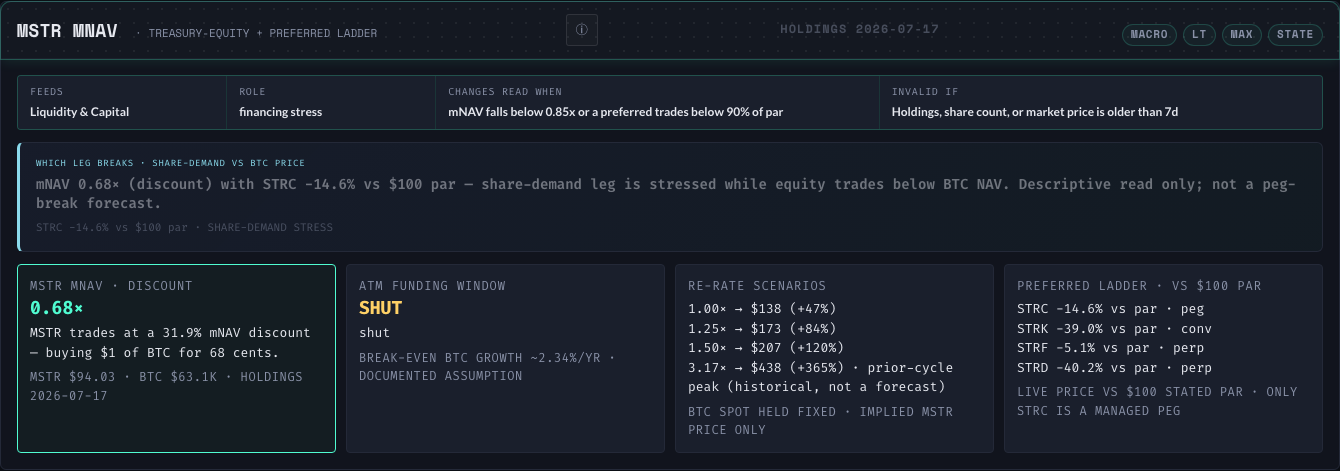

MSTR mNAVFeeds · Money

Strategy's diluted market value relative to its Bitcoin treasury value, plus preferred-share price and funding-health context.

Above 1× is a premium for leverage and capital access; below 1× is a discount. Neither automatically means cheap or expensive.

mNAV falls below 0.85× or preferred financing shows material stress.

Holdings, share count, or prices are older than seven days.

Supply DynamicsFeeds · Money

Illiquid and long-term-held supply trends, which estimate how much float is unavailable to trade.

Rising illiquid supply means absorption and tighter float. Falling illiquid supply means previously dormant supply is becoming available.

The trend reverses across two or more consecutive readings.

The holder series is unavailable or older than seven days.

Liquidity & CapitalFeeds · Money

A synthesis of ETF flows, deployable-liquidity pipeline, stablecoin and reserve flows, and holder absorption.

Positive and broad receipts mean capital is entering. A single positive component with quiet activity means weak participation, not full confirmation.

ETF, pipeline, and money-flow components align or materially diverge.

Feeds are empty, stale, or use incompatible time windows.

Entity RegimeFeeds · Money

Who is driving supply and demand across the same windows: long-term-holder supply, 7-day and 30-day ETF flow, corporate treasuries, and broad entity accumulation.

Start with the alignment label, then read each participant. “Recovering” means short-term ETF flow improved while the 30-day total remains negative; “split” means CryptoWatch will not force false confluence.

A major cohort changes stance or the four participant windows become aligned.

Coverage is missing, horizons are mixed without a label, or transfer activity is treated as confirmed selling.

Macro · permission and cross-asset context

Macro RegimeFeeds · Macro

M2 growth, dollar strength, real yields, Fed liquidity, yield curve, credit spreads, and BTC's cross-asset relationship.

Expanding money and easier financial conditions grant permission to bullish crypto signals. Dollar, rate, or credit stress can cap them.

Money, dollar, rates, or credit cross a declared regime boundary.

Monthly and daily inputs are compared without respecting freshness.

Capital RotationFeeds · Macro

Bitcoin's 30-day and 90-day relative performance versus semiconductors, Nasdaq, gold, and other macro risk assets.

BTC leadership suggests crypto-specific demand. Broad risk assets leading BTC suggests capital is available but not yet rotating into Bitcoin.

Bitcoin leads or lags the comparison basket across both windows.

Fewer than three benchmark legs are live.

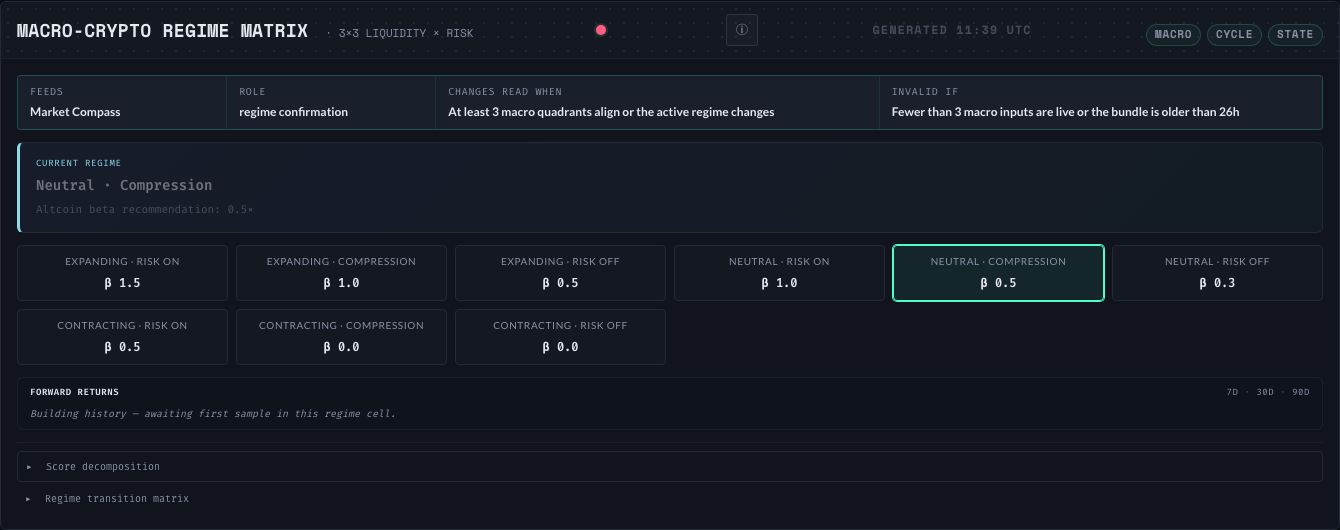

Macro-Crypto Regime MatrixFeeds · Macro

A 3×3 intersection of liquidity: expanding, neutral, contracting; and crypto risk: risk-on, compression, risk-off.

The same crypto signal means different things in different macro cells. Expanding plus risk-on supports exposure; contracting plus risk-off demands defense.

The active matrix cell changes or three macro quadrants align.

Fewer than three macro inputs are live.

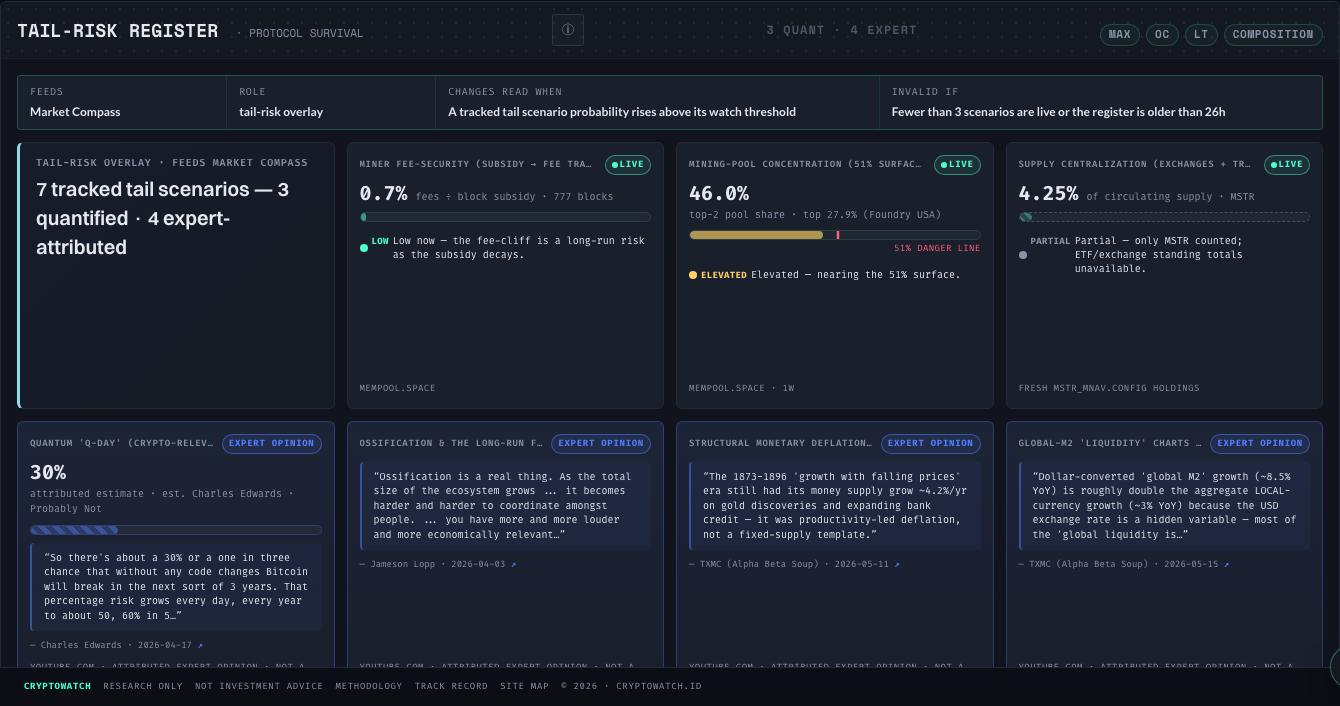

Tail-Risk RegisterFeeds · Macro

Low-frequency structural risks such as miner fee security, custody concentration, and protocol ossification.

These are thesis risks, not daily trading signals. Watch direction, threshold proximity, and whether several risks worsen together.

A tracked scenario rises above its declared watch threshold.

Fewer than three scenarios are live or the register is stale.

Action · timing, execution, and accountability

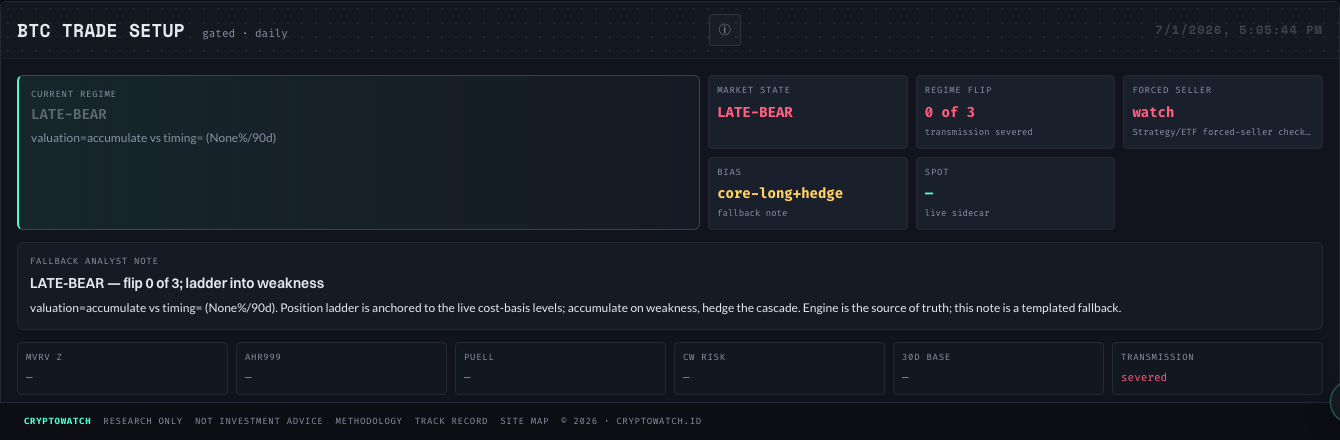

BTC Trade SetupFeeds · Action

A deterministic plan built from live cost-basis levels, position ladder, regime gates, risk limits, and historical base rates.

Read regime, allowed posture, entry ladder, invalidation, and sizing in that order. A withheld setup means the gates did not permit precision.

Price enters a declared zone while regime and risk gates permit exposure.

Entry, stop, sizing, or the supporting snapshot is stale or withheld.

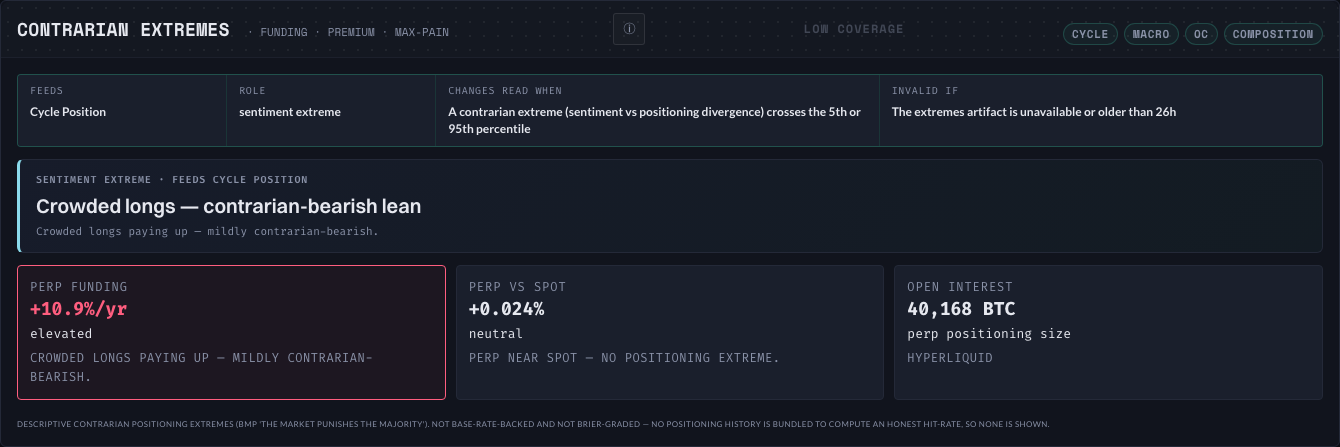

Contrarian ExtremesFeeds · Action

Extreme funding, spot premium, sentiment, options skew, and max-pain conditions where positioning becomes one-sided.

Extremes are reversal context, not immediate triggers. Look for divergence between fearful positioning and stabilizing price, or euphoric positioning and weakening spot.

An extreme crosses the 5th or 95th percentile with confirming price behavior.

The extremes artifact is stale or the signal lacks confirmation.

Execution LayerFeeds · Action

A synthesis of options volatility, perpetual funding, open-interest crowding, and estimated liquidation magnets.

Use it to time a thesis already supported by Cycle and Money. Crowded longs raise flush risk; crowded shorts can create squeeze fuel.

Funding, options, and liquidation positioning align around an extreme.

A component is missing or derivatives are used as a cycle call alone.

OptionsFeeds · Action

DVOL implied volatility, near-versus-far term structure, 25-delta skew proxy, and dealer-gamma strike clusters.

Backwardation signals near-term panic; low-volatility contango near highs can signal complacency. Negative skew means downside protection is expensive.

Volatility, term structure, skew, or gamma clusters enter an extreme.

The surface is stale or one thin expiry dominates.

Funding RegimeFeeds · Action

The payment between perpetual-futures longs and shorts, normalized to an annualized rate across the selected contract universe.

Positive means longs pay shorts; negative means shorts pay longs. Mild positive is normal. Very positive means crowded longs; deeply negative means crowded shorts.

Funding reaches an extreme, changes sign, or diverges from spot direction.

Low-volume contracts dominate, or carry is treated as guaranteed yield.

Liquidation LevelsFeeds · Action

Estimated forced-liquidation clusters above and below spot plus the nearest high-open-interest options pin.

Clusters above can fuel a short squeeze; clusters below can accelerate a long cascade. Use them as risk zones, not guaranteed price targets.

A large cluster or dealer pin is close enough to change entry, stop, or patience.

Estimated cluster size is mistaken for measured orders.

DCA Entry ZonesFeeds · Action

A precommitted allocation ladder anchored to realized-price and cohort-cost levels, with fixed capital percentages by zone.

Use zones to control cadence and dry powder. Deeper valuation zones permit larger tranches; they do not promise an immediate rebound.

Spot enters a new zone that has not already been deployed.

Realized price is missing or the same allocation is counted twice.

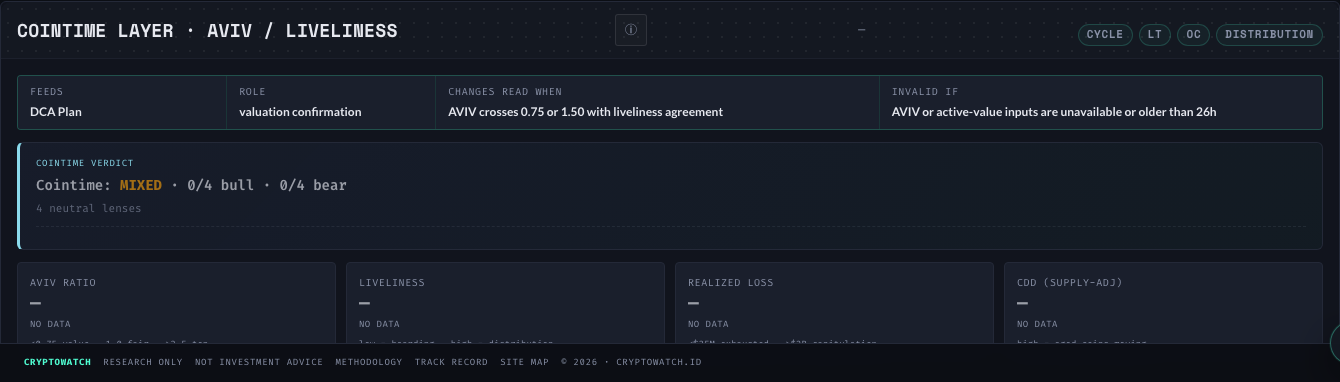

Cointime LayerFeeds · Action and Cycle

AVIV and liveliness, which weight valuation by economically active versus dormant coin supply.

Low AVIV suggests active-value compression; high AVIV suggests stretched valuation. Liveliness shows whether old supply is becoming active.

AVIV crosses 0.75 or 1.50 and liveliness agrees.

AVIV or active-value inputs are missing or stale.

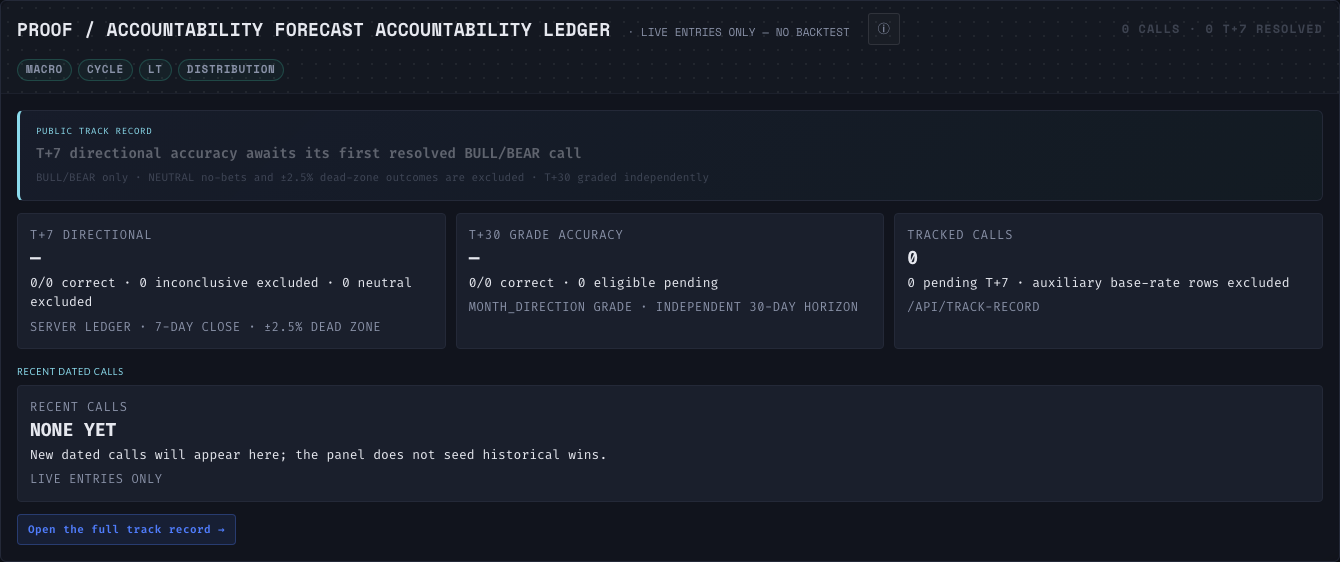

Forecast AccountabilityFeeds · trust

Resolved directional calls plus a separate daily receipt trail for every on-chain evidence family: observation count, state changes, persistence, regime, and later 7/30/90-day price context.

Use forecast calibration for actual calls. Use interpretation receipts to verify what the evidence said and when it changed. Forward returns beside descriptive states are context—not forecast wins.

A call resolves, or a daily evidence family changes state enough to alter the five-decision synthesis.

Descriptive state receipts are mislabeled as price predictions, or small samples are presented as proven reliability.

00About CryptoWatch

CryptoWatch is where serious crypto decisions get made.

Macro tells you if and when to be exposed — with scored inputs across macro, cycle, on-chain, and execution synthesized into a single verdict.

Desk keeps the thesis, sizing context, and accountability trail attached to that verdict.

One for the allocation decision. One for the operating discipline around it.

Macro — The Bitcoin Macro Cockpit

Macro is organized as a layered stack: Macro → Cycle → On-Chain → Execution. The synthesis screen is the apex — a single composite verdict built from the scored inputs that are live, with an explicit conflict resolver telling you when lenses disagree.

Macro shows what the data says, where the data disagrees, and what a disciplined allocator can do with that read.

Why we built this

Because the tools that exist are either raw data dumps (on-chain analytics platforms, exchange-flow services — here's 200 charts, figure it out) or black-box signals (pay us, trust us, we'll tell you when to buy). Neither respects how a thoughtful trader actually makes decisions.

A real cycle decision requires checking macro liquidity, cycle timing, on-chain stress, derivatives positioning, institutional flows, and sentiment — simultaneously. No single data source covers all of them. We wanted one screen that does, with a framework that explains exactly how each signal contributes to the verdict.

Why we're different

| Platform | What they give you | What CryptoWatch gives you |

|---|---|---|

| On-chain analytics platforms | Raw on-chain data. You build your own dashboard. | Pre-synthesized composite. Every indicator scored, weighted, and explained. |

| Cycle-chart aggregators | 200+ charts. Expert commentary. No single verdict. | One gauge, one number, one verdict — with the full breakdown visible if you want it. |

| Exchange-flow services | Exchange flows + alerts. Professional data tools. | Flows as one input among six layers. The verdict weighs flows against macro, cycle, and derivatives. |

| Charting platforms | Charts + indicators. You interpret everything. | Interpretation is the product. We take a position and show our work. |

| Paid signal groups | "Buy now." No reasoning. No accountability. | Full reasoning chain. Accuracy tracked publicly. Every call has a confidence level. |

Our specialty

Macro: Cycle intelligence, not day-trading signals. Built for the question "where are we in the 4-year BTC cycle?" and its practical follow-ups: should I be accumulating, holding, or distributing? At what size? With what conviction?

Desk: Thesis discipline, not a trade room. Built for the question "what would invalidate this allocation read?" and its follow-ups: what size is justified, what evidence matters, and what must be logged for accountability?

Mission

Make cycle intelligence and narrative alpha accessible. The data that drives billion-dollar fund decisions should be readable by anyone with 5 minutes a day and a browser.

Vision

A world where no retail crypto investor gets caught on the wrong side of a cycle turn — or chases a narrative peak — because they didn't have access to the right data in the right format at the right time.

Other platforms give you charts, raw data, and exchange flows. CryptoWatch gives you the verdict — and shows its work.

01What this is

cryptowatch.id is a live BTC cycle intelligence dashboard. It synthesizes macro, cycle, on-chain, and derivatives signals into a single composite gauge that outputs one of seven verdicts — from STRONG SELL to STRONG BUY — and shows you exactly which indicators are driving it.

The dashboard exists because most "crypto dashboards" pick one lens (just on-chain, just TA, just sentiment) and miss the rest. Real cycle turns happen when macro, cycle position, on-chain cohort behavior, and derivatives positioning all line up. We wanted a single surface that shows whether they do.

Every number on the dashboard is computed live from primary sources. Nothing is hand-entered. Nothing is hardcoded. If the backend pipeline goes down, the number goes stale and the UI says so.

This is not a signal service. It does not tell you when to buy or sell. It shows you what the underlying data says right now, in a single view, with all the math visible. The verdict is a summary of conditions, not a trade recommendation. Read the disclaimer.

02How to use the dashboard

A 6-step session workflow. Open the dashboard, go through these in order. Each step narrows the decision space until you have a concrete action (or confirm there's nothing to do).

Step 1 · Read the composite verdict (SIGNAL)

The first thing you see. The gauge sums 21 signed scores into a single number from −24 to +24 and maps it to one of 7 verdict bands. Read two things:

- Verdict + score. "MILD BUY +7" means conditions lean bullish but conviction is partial.

- Confidence %. If it's above 80%, indicators agree. If it's below 60%, the total is being driven by a few strong signals while the rest disagree — act smaller.

If the verdict is WAIT (score −2 to +1), stop here. Preserve dry powder. Don't force a trade out of boredom.

Step 2 · Check L4 Execution first (FUNDING + OPTIONS)

L4 is the trigger layer. It tells you whether the derivatives market is already crowded in one direction. This matters more than anything else for timing, because extreme positioning resolves in 1-4 weeks, not months.

- Funding < −54% annualized → shorts are overloaded. Contrarian long setup in place.

- Funding > +54% annualized → longs are overloaded. Contrarian short / top warning.

- DVOL > 90 → panic priced in. Historically coincides with bottoms.

- IV term backwardation → immediate fear priced in. 2020 COVID, 2022 FTX both had it at the low.

Step 3 · Verify with L3 On-Chain (TIER 1 + TIER 2)

L3 is the cohort layer. It answers: "is the on-chain population actually at a stress point, or is this just derivatives noise?" Open the Tier 1 panel and read the triggered count.

- 0/4 Tier 1 → no confirmed bottom. Cap any planned allocation at 30-40%.

- 1-2/4 Tier 1 → approaching. Start watching for the next trigger. Deploy first DCA tranche if Zone A price is hit.

- 3-4/4 Tier 1 → maximum on-chain confluence. Only happens at cycle bottoms in backtest. Deploy full allocation.

Tier 2 is the confirming layer — softer triggers like LTH MVRV < 1, US Spot Premium positive, Liveliness falling. Tier 2 alone isn't enough to act, but Tier 2 triggering while Tier 1 is still 1-2 of 4 is a leading signal that Tier 1 is about to fire.

Step 4 · Check L2 Cycle Position (CYCLE)

L2 is the slow map. It won't change between sessions — that's the point. Read:

- AVIV Ratio — where we sit in the post-ETF valuation band. <0.75 is historically extreme undervaluation.

- MA Stack Regime Score — 0/4 or 1/4 confirms bear regime. 4/4 confirms full bull.

- Halving regime — what phase the time-based calendar says we're in. If L2 says "late bear" and L3 says Tier 1 fires, conviction doubles.

- Bottom Proximity composite — the one-number summary of how close we are to the bottom zone.

Step 5 · Check L1 Macro permission (L1 MACRO)

L1 is the override layer. If macro is hostile, even extreme undervaluation can get cheaper. Read:

- M2 YoY > +3% → liquidity expanding. Full conviction in crypto-native signals.

- M2 YoY < −2% → liquidity contracting. Cap allocation regardless of how cheap on-chain looks.

- DXY +5% over 3m → dollar strengthening. Crypto fights a headwind. Reduce size.

- BTC-SPX 30d correlation high → macro dominates. Watch equities for direction.

2022 is the textbook reason L1 exists. On-chain screamed "cheap" for 6 months while DXY rallied 20% and crushed BTC another 40%. The framework's L1 layer would have capped your allocation during that window.

Step 6 · Map to DCA zones (DCA)

DCA translates the verdict + confluence into a concrete allocation. The dashboard computes 5 zones (A-E) live from Realized Price and historical multipliers. Your job:

- Never deploy all capital at once. Scale in across zones.

- Zone A (closest to current price) gets the smallest tranche. Zones D-E (deepest) get the largest — reserved for maximum confluence.

- When Tier 1 fires 3-4/4 inside Zone C or D, front-load the remaining allocation. That's the highest-conviction buy in the entire cycle.

Once you know the flow: 3-5 minutes a day. The point of a composite framework is that most of the work is already done for you. You're reading a verdict, verifying it against 2-3 confirming signals, and checking L1 for a veto. That's it.

02bDecision and evidence contracts

Context earns dashboard space only when it names the verdict it feeds, the threshold that can change that verdict, its invalidation condition, and its freshness boundary.

How to read a decision-contract rail

Twenty-two supporting panels now begin with the same four fields: Feeds names the primary decision owner; Role explains whether the panel confirms, times, filters, or executes that decision; Changes read when states the measurable escalation threshold; and Invalid if states when the panel must be ignored. The current synthesis line remains the live read; the rail is the stable methodology contract.

Machine-readable evidence services

The five former public evidence services (intraday delta, social emergence, mindshare, OSINT health, daily debate) were retired on 2026-07-15 with their Tier-C producer stack. They are not part of the current public contract.

03Four evidence questions behind five decisions

The framework asks four evidence questions across Macro, Cycle, On-Chain, and Execution. The Observatory synthesizes those answers into five user decisions: Now, Cycle, Money, Macro, and Action. Bitcoin State reconnects them into one complete thesis.

The permission layer. Macro doesn't tell you to buy or sell BTC. It tells you whether BTC-specific signals are allowed to work. When M2 is expanding and DXY is weakening, crypto-native bullish setups resolve normally. When the opposite is true, they get overwhelmed by capital flight. L1 is the binary that decides whether the other 3 layers matter.

The slow map. This layer barely changes week-to-week. It tells you which phase of the 4-year halving cycle we're in: accumulation, markup, distribution, or bear. L2 is the context that determines what L3 and L4 readings actually mean. A funding spike at day 480 post-halving means distribution is starting. The same funding spike at day 950 post-halving means shorts are capitulating.

The behavioral layer. This is BTC's unique advantage over every other asset — we can see what every holder cohort is actually doing on-chain. L3 tells you whether long-term holders are hoarding or distributing, whether short-term holders are in profit or underwater, whether miners are capitulating, whether institutional spot flows are positive. L3 is where the real bottom and top signals live.

The trigger layer. The fastest-moving layer. L4 reads the derivatives market for crowded positioning — funding rates, open interest, implied volatility, skew. L4 won't call a cycle bottom by itself. But it's what separates a 6-week-early call from a same-week entry. When L2 and L3 say "bottom is close" and L4 says "shorts are at −190% annualized funding," that's the moment.

These four evidence layers are read in sequence when signals conflict:

- L1 wins overrides. Hostile macro caps any bullish call, no matter how strong L2-L4 are.

- L2 defines the playbook. L3/L4 are read differently depending on cycle phase.

- L3 provides the evidence. Without L3 confirmation, L4 alone is just "crowded positioning" — not a bottom call.

- L4 provides the timing. When L2 and L3 both say yes, L4 is what you watch for the entry trigger.

Out-of-sample validation note

This framework was designed and backtested on BTC data from 2015-2025, covering three full cycles (2015 bottom, 2018 bottom, 2022 bottom) and one cycle top (2025 ATH). Every threshold, every verdict band, every regime boundary was calibrated to fit these cycles. The 2026-2029 cycle is the first true out-of-sample test.

This is more honest than most crypto tools but it means the framework's historical track record — while real — is in-sample. Treat forward readings as probabilistic signals, not guaranteed calls. Per audit v2 #19.

04The 4-layer framework

Every composite on the dashboard rolls up through four layers. Each layer answers a different question. Each contributes signed scores that sum into a single composite.

L1 · Macro Regime

Question: is the global environment supportive of risk assets, or is it pulling capital out?

Bitcoin does not exist in a vacuum. When the US dollar strengthens and global liquidity contracts, even a perfect on-chain setup struggles. When M2 is expanding and DXY is rolling over, the same on-chain setup becomes a launchpad. L1 is the permission slip.

Signals: US M2 year-over-year · DXY 3-month change · BTC–SPX 30-day correlation regime.

L2 · Cycle Position

Question: where are we in the 4-year Bitcoin cycle — capitulation, accumulation, markup, or distribution?

Cycle position is the slow-moving map underneath everything else. It blends time-based features (halving framework), technical regime (weekly MA stack), valuation (AVIV Ratio from Cointime Economics), and composite bottom-proximity scoring. This layer is what separates a "dip" from a "bottom" and a "pullback" from a "top."

Signals: MA Stack Regime Score · AVIV Ratio · Halving regime · Bottom proximity composite · Drawdown from ATH.

L3 · On-Chain Stress

Question: is the on-chain population under stress, taking profits, or still distributing?

L3 is the cohort layer. It reads what long-term holders and short-term holders are actually doing on-chain, separates them by age, measures profit/loss behavior, and tracks institutional flow through spot ETF activity and US spot premium. This layer catches real bottoms before price does.

Signals: Zero-FP Tier 1 confluence · LTH MVRV · STH MVRV · Liveliness / Vaultedness · Realized Loss · US Spot Premium · IBIT activity multiplier · LTH SOPR.

L4 · Execution Timing

Question: is now the actual moment — is derivatives positioning primed to squeeze, or is the crowd already one-sided?

L3 says "a bottom is close." L4 says "and shorts are max-crowded at -70% annualized funding with backwardated IV." That's the difference between a six-week early call and a same-week entry.

Signals: BTC funding annualized · DVOL · IV term structure shape · 25Δ skew proxy · OI / market cap.

06The composite gauge

Every indicator contributes a signed score in the range −2 to +2 by default. After layer-strength multipliers (see "Multipliers and bounds" below) the per-indicator score is clamped to ±3. The 21 scored indicators sum, the running total is clamped to ±24 for display, and that total maps to one of seven verdict bands.

The scoring convention

+2 = strongly bullish (extreme undervaluation, capitulation, panic, or crowded short positioning).

+1 = mildly bullish (undervalued or supportive).

0 = neutral / no signal.

−1 = mildly bearish (overvalued or stretched).

−2 = strongly bearish (euphoric distribution, crowded long positioning, or extreme complacency).

Multipliers and bounds (Round 2 audit clarification, 2026-05-03)

The naive sum of 21 × ±2 would be ±42. The dashboard caps the displayed total at ±24 via two mechanisms:

- Per-indicator post-multiplier clamp at ±3. Cycle phase context (e.g. confirmed bottom-cluster) applies a layer-strength multiplier to indicators in the relevant layer; the boosted score is clamped to ±3 to preserve a bounded invariant. So an L3 indicator scoring +2 raw can read as +3 in a confirmed bottom-cluster regime, but no further. Reference implementation:

cw_macro.htmlaggregator,boosted = score × layerMult; r.score = clamp(boosted, -3, +3). - Display clamp at ±24. The summed total is clamped to ±24 in the gauge fill / verdict-band lookup. Scores that would otherwise saturate above ±24 are flagged in tooltips but are rare in practice — the effective historical range across 11 years of cycle data is ~−12 to +14 (see "Effective range" note in §LTH).

- Theoretical max ≠ display range. The gauge is not calibrated to ±42 because (a) indicators rarely score at extreme values simultaneously across all 21 lenses, and (b) verdict bands were tuned against actual historical extremes, not theoretical ones. The ±24 display range is a calibrated band, not a hard physics-of-the-system limit.

Verdict bands

| Score range | Verdict | Meaning |

|---|---|---|

| ≥ +16 | STRONG BUY | Multiple layers at capitulation extreme, derivatives crowded short, high-conviction bottom window |

| +8 to +15 | BUY | Cycle + on-chain both align bullish, derivatives not yet fighting the setup |

| +2 to +7 | MILD BUY | Conditions lean bullish but conviction is partial — one or two layers still neutral |

| −1 to +1 | WAIT | Indicators disagree or cancel out — no edge |

| −2 to −7 | MILD SELL | Conditions lean bearish — late-cycle risk appearing in one or two layers |

| −8 to −15 | SELL | Cycle + on-chain align bearish, derivatives confirm distribution |

| ≤ −16 | STRONG SELL | Multiple layers at euphoric extreme, high-conviction top window |

Confidence

Alongside the score, the gauge shows a confidence percentage. This is a coverage + agreement score:

- 50% from coverage — what fraction of the 21 indicators have live data right now (if a data feed is stale, its indicator drops out).

- 50% from directional agreement — of the indicators that have data, what fraction are scoring in the same direction as the total.

A +8 score with 90% confidence means "most indicators agree and most of them have fresh data." A +8 score with 55% confidence means "the total is being driven by a few strong signals while the rest are neutral or conflicting."

What the gauge is not

The composite score is not probabilistic. A +17 STRONG BUY does not mean "71% chance of going up." It means "conditions match historical bottom setups." Historically those setups have preceded multi-month rallies — but Bitcoin has done things that have never happened before, and will again. Use the gauge as a synthesis of conditions, not a win-rate.

07Confluence decision rules

The gauge is the one-number summary. The decision rules are what you do when you actually have to act. This section is what separates reading the dashboard from using it.

When layers agree — act with full size

All 4 layers aligned is the highest-conviction setup. It happens maybe 3-5 times per 4-year cycle. When it does, the signal is unambiguous.

L1 Macro: M2 starting to re-expand, DXY rolling over from +20% peak → +1

L2 Cycle: MA Stack 0/4, AVIV 0.67, halving regime late bear, drawdown −77% → +7

L3 On-Chain: Tier 1 4/4 triggered, LTH MVRV 0.82, LTH SOPR 0.78, realized loss $18M/day → +7

L4 Execution: BTC funding −190% annualized, DVOL 94, IV backwardation, 25Δ skew −12 → +2

Composite: +17 STRONG BUY. Every indicator except a few L1 variables at or near maximum confluence.

Action: deploy Zones C-D-E aggressively (50-100% of remaining allocation). Set 12-18 month hold horizon. Do not try to time further dips.

When L4 conflicts with L2+L3 — reduce size, wait

The most common edge case: on-chain and cycle position agree there's an accumulation zone approaching, but derivatives positioning is on the wrong side. This is usually resolved by a liquidation event — don't deploy before it happens.

L1: M2 contracting, DXY +15% YTD → −2

L2: AVIV dropping toward 0.75, halving regime mid-bear → +3

L3: Tier 1 1/4 triggered (MVRV briefly crossed <1 on LUNA collapse), NUPL barely negative → +1

L4: Funding still positive, OI/Mcap at 3.8% (overleveraged), no panic in IV → −1

Composite: +1 WAIT. Framework said wait.

Why the framework was right: Only 1 of 4 Tier 1 signals fired. L4 showed overleveraged longs still in place. Real bottoms need L4 capitulation — which came 5 months later at FTX.

The lesson: never act on 1-2 Tier 1 signals. All 4 must fire. The confluence requirement is what made the framework skip June 2022 and catch November 2022.

When L1 is hostile — override everything

Macro headwind delays even extreme undervaluation. This is the hardest rule to follow emotionally because on-chain will be screaming "cheap" while price keeps dropping.

AVIV dropped below 0.80 (historical accumulation territory) in July 2022. On-chain metrics suggested the bottom was near. But M2 was contracting at −1.5% YoY and DXY was at +18% 3-month change. L1 was maximally hostile.

What actually happened: BTC fell from $22K in July to $15.5K in November — another 30% downside. The framework's L1 veto would have capped allocation at 30-40%, preserving dry powder for the real bottom.

Rule: when L1 is hostile (M2 contracting AND DXY rising), cap total allocation at 30-40% of planned size regardless of L2/L3. Wait for L1 to flip before deploying the rest.

Layer priority hierarchy

| Condition | Override rule |

|---|---|

| L1 Macro hostile (M2 YoY < −2% AND DXY 3m > +5%) | Cap allocation at 30-40% regardless of L2/L3 strength |

| L4 Funding > +54% annualized | Never add longs. Reduce existing if L3 is also weakening |

| L4 Funding < −54% annualized | Adds conviction if L2+L3 already support. Not sufficient alone. |

| L3 Tier 1 count = 0/4 | Maximum 40% of planned allocation. Not a bottom yet. |

| L3 Tier 1 count = 1-2/4 | Up to 60% of planned allocation. Start scaling in. |

| L3 Tier 1 count = 3-4/4 | Full planned allocation permitted. Historical cycle-low territory. |

| L2 AVIV < 0.75 | Highest-conviction buy zone regardless of short-term noise |

| L2 MA Stack 4/4 + AVIV > 2.0 | Distribution has begun. Size down 20% per week until AVIV < 1.5 |

| L2 halving regime = distribution_danger | Default to caution even if L3/L4 look bullish. Top window. |

The rules above are intentionally more conservative about adding risk than about preserving capital. Missing a cycle bottom by 10% is annoying. Deploying full size 3 months before the real bottom costs 30-40%. The rules optimize for the second mistake, not the first. You will feel slow. That's the price.

05Framework design rationale

Why 21 indicators and not 10. Why ±2 scoring and not raw values. Why some indicators are symmetric and some aren't. Why the verdict bands land at ±16 and ±8. These are not arbitrary choices — they're deliberate decisions with backtest rationale.

Why 21 indicators

The framework needs to cover 4 independent dimensions (macro, cycle, on-chain, execution) without missing signal and without becoming noise. We landed on 21 after testing configurations from 8 to 35. The distribution:

- 3 macro (M2, DXY, BTC-SPX correlation) — thin, because macro signals move slowly. More macro indicators adds redundancy without signal. 3 is enough to detect the regime.

- 5 cycle (MA Stack, AVIV, Halving regime, Bottom Proximity, Drawdown) — our highest-credit layer. Each indicator uses a different methodology (technical / valuation / time-based / composite / price) so they're uncorrelated enough that all 5 contribute independent signal.

- 8 on-chain (Tier 1 confluence, LTH MVRV, STH MVRV, Liveliness, Realized Loss, US Spot Premium, IBIT activity, LTH SOPR) — biggest layer because on-chain is BTC's native data advantage. We want cohort behavior, valuation, miner stress, institutional flow, and profit-taking dynamics all covered.

- 5 execution (Funding, DVOL, IV term, 25Δ skew, OI/Mcap) — enough to capture derivatives positioning without making L4 dominate.

Fewer than 21 leaves blind spots. In testing, 15-indicator versions consistently missed either miner capitulation signals or IV term structure reversals. More than 21 crosses into diminishing returns — each additional indicator contributes less signal while adding correlated noise and computation load. 21 is where backtest accuracy plateaus.

Why ±2 scoring instead of raw values

Every indicator uses different units. M2 YoY is a percentage. MVRV is a dimensionless ratio. Realized Loss is dollars per day. Funding is an annualized percentage. You can't sum them directly. A normalized score per indicator (−2 extreme bearish to +2 extreme bullish, 0 neutral) makes them addable and comparable.

Why specifically ±2 and not ±1 or ±3?

- ±1 is too coarse. Only 3 states per indicator (bearish / neutral / bullish). Loses the "extreme" signal that is exactly what we care about at cycle turns.

- ±2 gives 5 states: extreme bearish, mildly bearish, neutral, mildly bullish, extreme bullish. This matches how humans naturally categorize conditions. "Cold, cool, mild, warm, hot" is the psychological template.

- ±3 or more over-weights noisy indicators. Funding can move 100% in a single day. Rewarding it +3 for a temporary spike would let it dominate the composite. The ±2 cap keeps any single indicator from owning more than ~8% of the theoretical range.

Why some indicators are asymmetric

Not every indicator scores symmetrically. Some push harder in one direction than the other. These aren't bugs — they're deliberate.

| Indicator | Range | Why asymmetric |

|---|---|---|

| M2 YoY | −2 to +1 | Contracting M2 is a deep structural headwind — worth full −2 weight. Expanding M2 is a tailwind but never a trigger by itself, so +1 is enough. |

| DXY 3m | −1 to +1 | DXY is a regime context, not a direct trigger. Capped at ±1 so it can't dominate crypto-native signals. |

| BTC-SPX 30d correlation | 0 only | Pure regime indicator — tells you which other indicators matter. Never directional. Always scored 0. |

| Drawdown from ATH | −1 to +2 | Being near ATH isn't automatically "sell" (bull markets stay near ATH for months). But a >70% drawdown is strongly bullish because every historical cycle bottom had one. |

| Tier 1 triggered count | −1 to +2 | 0/4 just means "no bottom signal active right now" — not "sell." It's neutral-to-mildly-cautious. But 3-4/4 is historically unique to final cycle lows, so it deserves the full +2. |

| DVOL | −1 to +2 | High DVOL = panic priced in = historically coincides with bottoms, full +2. Low DVOL is only mildly bearish (complacency warning, not a top signal by itself). |

| IBIT Activity Multiplier | −1 to +2 | Activity surges happen at both tops (FOMO) and bottoms (panic buying). Needs L2 context to read direction. Capped upside so it can't drive the composite alone. |

How the verdict bands were calibrated

The 7 bands (−24 to +24) were calibrated with offline historical backtests against cycle extremes since 2015.

| Range | Verdict | Historical backtest |

|---|---|---|

| ≥ +16 | STRONG BUY | 2015-01-14 bottom (+19), 2018-12-15 bottom (+18), 2022-11-21 FTX bottom (+17). 3 of 3 major cycle bottoms landed in this band. |

| +8 to +15 | BUY | Mid-accumulation phases, 4-6 months after final lows. Strong conviction but not max confluence. |

| +2 to +7 | MILD BUY | Early accumulation, partial setup. Current 2026-04-14 reading sits here at +7. |

| −1 to +1 | WAIT | Indicators disagree or cancel out. No edge. Dry powder. |

| −2 to −7 | MILD SELL | Early distribution warnings. |

| −8 to −15 | SELL | 2021-04-14 first top, 2025-08 pre-top. Distribution confirmed. |

| ≤ −16 | STRONG SELL | 2021-11-09 cycle ATH (−18). 2025-10-06 ATH landed at −8 because the 2025 top was shallower than prior cycles (diminishing extremes). |

The ±16 threshold is where the framework has >80% historical precision for "this is a cycle turn." The ±8 threshold is the "conviction grows" line. ±2 is the noise floor — anything inside is a WAIT.

The 2025 cycle top only scored −8 (SELL, not STRONG SELL) because post-ETF cycle extremes are milder than pre-2024 cycles. This is the "diminishing extremes" thesis — each cycle's peaks and troughs move closer to the mean because institutional flows dampen volatility. The framework handles this automatically via the asymmetric Tier 1 count and the AVIV Ratio (which itself accounts for institutional realized cap). We expect future tops to land in the −8 to −14 range rather than the −18+ range of 2021.

08Indicator reference

Every scored indicator, in order, with its endpoint, logic, and scoring bands. This is the full source-of-truth for what the dashboard is computing.

L1 · Macro Regime

M2 Year-over-Year (US) L1

US M2 money supply year-over-year change. The slow-moving global liquidity oscillator. BTC cycle highs correlate strongly with M2 expansion peaks; cycle lows correlate with M2 bottoms.

BTC has had a ~80% rolling correlation with global M2 liquidity since 2013. Crypto is a long-duration, risk-on asset that breathes in lockstep with the money supply. When M2 expands, risk capital flows into the longest-duration assets (tech stocks, emerging markets, crypto). When M2 contracts, the flow reverses. M2 isn't a trigger — it's the permission slip.

We use US M2 as a proxy for global liquidity because it's the largest single component and updates weekly. The ideal indicator would blend US M2 + ECB M2 + PBOC M2 but the correlations are tight enough that US alone captures the regime.

| Date | M2 YoY | BTC context |

|---|---|---|

| 2020-06 | +24.7% | Fed pandemic QE — start of the 2020-2021 bull run |

| 2021-11 | +13.1% | Peak of 2021 bull + cycle ATH |

| 2022-06 | +5.9% | Fed tightening — LUNA collapse, M2 growth decelerating |

| 2022-12 | −1.3% | First M2 contraction in decades — coincided with cycle low |

| 2024-04 | +0.7% | Halving + post-contraction stabilization |

M2 is slow — it reflects economic conditions with a 3-6 month lag. When M2 starts contracting, BTC often rallies for another 2-3 months before capitulating. Conversely, M2 re-expansion can lag the cycle bottom by weeks.

Mitigation: never use M2 as a timing signal. Use it as a context filter — cap allocation sizes when M2 is contracting, full size when M2 is expanding. The timing comes from L3 + L4.

| Condition | Reading | Score |

|---|---|---|

| Accelerating positive | YoY > +3.0% | +1 |

| Positive but decelerating | 0% < YoY ≤ +3.0% | 0 |

| Flat / declining | −2.0% < YoY ≤ 0% | −1 |

| Contracting | YoY ≤ −2.0% | −2 |

DXY 3-Month Change L1

Dollar Index 3-month percent change. A strengthening dollar pulls capital out of risk assets; a weakening dollar fuels them. Historically the cleanest macro wind at BTC's back is DXY rolling over after a multi-month rally.

The US Dollar Index has the cleanest inverse correlation with BTC of any single macro variable. A rising dollar pulls global capital into USD-denominated assets (Treasuries, US equities). A falling dollar pushes capital into risk assets. The 3-month change captures the trend without reacting to daily noise.

We use DXY instead of the trade-weighted dollar because it's more liquid, updates in real time, and captures the same signal. The 3-month lookback is long enough to filter weekly chop but short enough to flag regime changes within a cycle.

| Date | DXY 3m | BTC context |

|---|---|---|

| 2022-07 | +7.2% | DXY rally crushed risk assets. BTC fell from $30K to $19K. |

| 2022-11 | +1.1% | DXY peak. BTC cycle low 2 weeks later. |

| 2023-01 | −4.8% | DXY rolling over. BTC bottomed, started recovery. |

| 2024-04 | +1.2% | Halving-week DXY stable. Neither tailwind nor headwind. |

| 2025-09 | +3.1% | Pre-cycle-top DXY strength. Distribution warning. |

DXY weakness can coexist with weak BTC during risk-off regimes (2018 bear market, DXY was flat-to-weak but BTC fell 84%). DXY is a necessary but not sufficient condition for BTC strength.

Mitigation: DXY is scored ±1 max (not ±2) precisely because it's a soft regime indicator. It can't drive the composite alone — it amplifies or dampens crypto-native signals.

| Condition | Reading | Score |

|---|---|---|

| Dollar strengthening (risk-off) | Δ3m > +2.0% | −1 |

| Range-bound | −2.0% ≤ Δ3m ≤ +2.0% | 0 |

| Dollar weakening (risk-on) | Δ3m < −2.0% | +1 |

BTC–SPX 30-Day Correlation L1

Rolling 30-day correlation between BTC and the S&P 500. This is a regime indicator, not a directional one. When correlation is high (>0.6), BTC is moving with risk assets and macro dominates. When correlation is low or negative, BTC is trading on its own narrative. Reported as context only — scored neutral (0).

This isn't a directional signal — it's a regime classifier. When BTC-SPX correlation is high (> 0.6), BTC is trading as a risk asset and macro conditions dominate. When correlation is low or negative, BTC is trading on its own narrative (halving, ETF flows, on-chain events) and L3 signals matter more.

We keep it in the framework scored at 0 (no direct composite contribution) because its job is to tell you which other indicators to weight heavily. High correlation → L1 Macro matters more. Low correlation → L3 On-Chain matters more. It's a meta-indicator.

| Date | Corr | Regime |

|---|---|---|

| 2020-03 | 0.92 | COVID crash — crypto sold as risk asset, maximum correlation |

| 2021-02 | 0.28 | Crypto-native bull — BTC decoupled, halving narrative dominant |

| 2022-06 | 0.78 | Macro bear — BTC tracked tech stocks down on every Fed meeting |

| 2024-01 | 0.35 | Spot ETF narrative — BTC decoupled from macro |

| 2025-03 | 0.51 | Mid-cycle, neither regime clearly dominant |

Correlation alone doesn't tell you direction. High correlation to a falling SPX is bearish; high correlation to a rising SPX is bullish. Mitigation: always read correlation alongside DXY and the SPX trend itself. The indicator is scored 0 by design — it only changes how you read the other indicators.

Fed Balance Sheet (WALCL) L1

Federal Reserve total assets ($T). QE = Fed buying bonds = liquidity injected into markets = risk-asset tailwind. QT = Fed running off holdings = liquidity drained = risk-asset headwind. Often called "THE most important macro signal for crypto" because BTC's multi-year cycles line up with Fed balance sheet expansion and contraction.

4w change: ≥+0.5% = QE (risk-on), −0.5% to +0.5% = stable, ≤−0.1% = QT mild, ≤−0.5% and 52w ≤−2% = QT accelerating (strongest headwind). Weekly series released Wednesdays; 4-row lookback ≈ 4 weeks.

Yield Curve · 10Y − 2Y (T10Y2Y) L1

Difference between the 10-year and 2-year US Treasury yields. Inversion (spread < 0) preceded every US recession since 1955 with a ~12-month lead. Crypto, being a long-duration risk asset, typically follows the risk-asset cascade 6-18 months after inversion normalizes upward.

<0pp = inverted (recession warning), 0-0.5 = flat, 0.5-2.0 = normal, >2.0 = very steep (post-recession recovery signature). We surface "days since sign flip" so you can gauge how fresh the current regime is.

Reverse Repo (RRPONTSYD) L1

Money market funds park cash at the Fed's overnight reverse repo facility — effectively removing it from risk markets. Peak was ~$2.5T in late 2022; drained below $1B through 2025. Draining RRP = capital flowing back into markets (risk-on tailwind); absorbing RRP = flight-to-safety (risk-off drag). $100B/30d is historically meaningful; $20B/30d matters in the current low-balance regime.

Real Yield · 10Y TIPS (DFII10) L1

Inflation-adjusted return on a 10-year Treasury — the opportunity cost of holding non-yielding crypto. Negative real yields = TradFi can't beat inflation = strong crypto tailwind (2020-2021 cycle). >2% = restrictive, meaningful crypto headwind (2024 environment).

<−1pp deeply negative (strong tailwind), −1 to 0 accommodative, 0 to 1 neutral, 1 to 2 tight, >2 restrictive (heavy headwind).

HY Credit Spread (BAMLH0A0HYM2) L1

The risk-appetite thermometer. Widening HY spreads = credit stress = risk-off across all assets. Crypto mirrors HY credit cycles tightly — during 2022's credit crunch HY blew out and BTC drew down with it; 2024's narrowing spreads coincided with BTC's rally to new highs.

<3% complacency (risk-on bias), 3-5% normal, 5-8% stressed (risk-off), >8% crisis.

VIX · Volatility Index (VIXCLS) L1

The classic "fear gauge." Sub-15 = complacency (historically precedes corrections), 20-30 = caution, >40 = panic. Crypto tends to follow VIX spikes into drawdown and recover on VIX collapse — the intraday sentiment specialist of the macro stack.

Dr. Copper (HG) L1

Industrial metals bellwether. Copper is consumed everywhere — construction, EVs, grid, electronics — so its price tracks global growth expectations. Rising copper = cyclical demand expansion (risk-on for crypto); falling = recession whispers. 90d horizon because copper is noisy day-to-day.

>+8% strong growth, +2 to +8 expanding, −2 to +2 neutral, −8 to −2 contracting, <−8 recession-like.

USD/CNY · China Capital Flow L1

CNY weakening vs USD historically signals Chinese capital outflow pressure — a bearish crypto signal since a material share of crypto flow has historically come through Asia. CNY strengthening = inflow signal. Small moves matter: 1.5% in 30d is notable for a managed currency like CNY.

L2 · Cycle Position

MA Stack Regime Score L2

Count of how many of the four weekly moving averages BTC is above (0/4 to 4/4). This is the primary backtest-validated technical regime signal from the Indicator Deep Dive framework. 0/4 matches the 2015, 2018, and 2022 cycle bottoms exactly. 4/4 matches every cycle top.

The simplest possible regime detector. No calibration, no window choice, no parameter tuning — just "is BTC above or below each long-term MA?" The lack of tuning is the point: every cycle low since 2015 had a 0/4 reading and every cycle top had a 4/4 reading. Zero false positives on the full stack transition.

We use 20/50/100/200 week windows because they span roughly 5 months to 4 years of price history, capturing everything from mid-cycle corrections to the full halving cycle. Daily MAs would be too noisy. Monthly MAs would be too slow.

| Date | MA Stack | BTC | What happened next |

|---|---|---|---|

| 2015-01-14 | 0/4 | $171 | +117× in 35 months |

| 2017-12-17 | 4/4 | $19,500 | −84% over 12 months |

| 2018-12-15 | 0/4 | $3,194 | +4.3× in 6 months |

| 2019-06 | 2/4 → 1/4 | $13,800 | −52% back to $6,600 (the 2/4 ambiguity case) |

| 2022-11-21 | 0/4 | $15,479 | +4.7× in 12 months |

| 2025-10-06 | 4/4 | $124,714 | −40% over 6 months (current cycle) |

2/4 is the genuinely ambiguous state. In 2019, the stack recovered from 0/4 → 2/4 → back to 0/4 before the real cycle turn. A trader treating 2/4 as a buy signal would have been stopped out.

Mitigation: we score 2/4 as 0 (neutral) precisely because it's ambiguous. The framework waits for 3/4 + at least one L3 confirmation before treating an MA Stack recovery as a real cycle turn.

| Regime | Reading | Score |

|---|---|---|

| Full bear (max DCA zone) | 0/4 | +2 |

| Late bear (bottom window) | 1/4 | +2 |

| Transition | 2/4 | 0 |

| Bull | 3/4 | −1 |

| Full bull (top zone) | 4/4 | −2 |

AVIV Ratio L2

The post-ETF replacement for MVRV Z-Score. Cointime Economics (Ark Invest + on-chain analytics, 2023) reweights supply by coin age to avoid the distortion that large dormant stashes create in classic realized cap. AVIV is what drives the Cointime Accumulation Score on the dashboard.

AVIV (Active Value / Investor Value) replaces classic MVRV Z-Score for the post-ETF era. The reason: institutional flows after January 2024 pushed large amounts of BTC into dormant custody (BlackRock's IBIT, Fidelity's FBTC, MicroStrategy). These holdings inflate the classic realized cap without reflecting real market activity, which distorts MVRV Z readings by 15-30%.

AVIV reweights supply by coin age so dormant institutional stashes don't drown the signal. The method comes from the 2023 Cointime Economics paper, which defined the approach specifically to solve the institutional-dormancy problem.

| Date | AVIV | Zone |

|---|---|---|

| 2015-01 | 0.42 | Extreme undervaluation (cycle low) |

| 2017-12 | 4.2 | Cycle top (2017 peak) |

| 2018-12 | 0.55 | Cycle low |

| 2021-11 | 3.1 | Cycle top |

| 2022-11 | 0.67 | Cycle low (2022) |

| 2025-10 | 1.56 | Cycle top (2025) — diminishing extremes! |

| 2026-04 | 0.953 | Current (accumulation zone) |

The 2025 top only reached AVIV 1.56 — far short of the 2.5 "top zone" threshold derived from pre-ETF cycles. This is the diminishing extremes problem: post-ETF cycles will likely never see AVIV above 2.0 again because institutional flows dampen the volatility.

Mitigation: treat AVIV > 2.0 as the new "late bull warning" threshold (not 2.5). When AVIV crosses 2.0 + other distribution indicators fire, that's the real top signal now. Don't wait for 2.5.

| Condition | Reading | Score |

|---|---|---|

| Extreme undervaluation | AVIV < 0.55 | +2 |

| Deep accumulation | 0.55 ≤ AVIV < 0.75 | +2 |

| Accumulation zone | 0.75 ≤ AVIV < 1.00 | +1 |

| Mid bull / hold | 1.00 ≤ AVIV < 1.50 | 0 |

| Late bull / trail stops | 1.50 ≤ AVIV < 2.50 | −1 |

| Cycle top zone | AVIV ≥ 2.50 | −2 |

Halving Regime L2

Time-based cycle phase. Maps days-since-halving to one of eight phases from early markup through distribution danger to late accumulation. This is pure time-of-cycle context; it's not price-dependent. When the halving regime and on-chain regime agree, conviction is highest.

BTC's supply schedule is the only deterministic structural feature of the asset. Every ~4 years the block subsidy halves, creating a predictable supply shock. Every cycle since 2012 has followed the same phase sequence: markup → distribution → bear → accumulation, anchored to halving day.

The exact phase boundaries (in days post-halving) were fit to the 2012, 2016, and 2020 halving cycles. The 2024 cycle is currently tracking inside the historical envelope for all three phases so far — peak at day 534 matched the 480-600 window, bear started on schedule.

| Cycle | Halving | Peak (day) | Bottom (day) |

|---|---|---|---|

| Cycle 1 | 2012-11-28 | day 367 (Dec 2013) | day 793 (Jan 2015) |

| Cycle 2 | 2016-07-09 | day 529 (Dec 2017) | day 892 (Dec 2018) |

| Cycle 3 | 2020-05-11 | day 548 (Nov 2021) | day 928 (Nov 2022) |

| Cycle 4 | 2024-04-20 | day 534 (Oct 2025) | projected day ~940-980 (Nov 2026 - Jan 2027) |

This is a time-based model — it's right about the window, not the exact date. Real cycle turns can be 30-60 days early or late. And the pattern could break in any single cycle (that's the nature of a 4-point regression).

Mitigation: pair with data-driven signals (Bottom Proximity, Tier 1, AVIV). When the halving regime and on-chain evidence agree, conviction is highest. When they disagree — specifically when data says "bottom" but time says "still early" — wait for data to catch up rather than front-running the clock.

| Phase | Score |

|---|---|

| early markup | −1 |

| markup | −1 |

| late markup | −2 |

| distribution danger | −2 |

| early bear | 0 |

| mid bear | +1 |

| late bear | +2 |

| accumulation extended | +2 |

Bottom Proximity Composite L2

A composite score (0–100%) that synthesizes multiple cycle-bottom signals — realized price proximity, MVRV/NUPL levels, drawdown depth, and cohort behavior — into a single "how close are we to a cycle bottom" reading. 0% = euphoric top. 100% = max capitulation confluence. Historical 2022-11-21 reading: 71%. Historical 2025-10-06 ATH reading: single digits.

A single 0-100 number that synthesizes every bottom-relevant signal we track: MVRV ratio, NUPL, Puell Multiple, Supply-in-Profit, drawdown depth, cohort behavior (LTH MVRV, Liveliness), realized price proximity. Each subscore is weighted by its historical reliability at calling cycle lows.

The goal is one-glance orientation. The ±24 gauge tells you the verdict; Bottom Proximity tells you how close we are to the bottom zone on a pure "cheapness/stress" axis. At cycle bottoms the value hits 80-95%. At cycle tops it drops to 5-15%.

| Date | Bottom Proximity | Zone |

|---|---|---|

| 2015-01-14 | 94% | Max capitulation |

| 2018-12-15 | 89% | Bottom zone |

| 2021-11-09 | 7% | Top zone (distribution) |

| 2022-06-18 | 54% | Mid bear — the June false signal (flagged "approaching" not "bottom") |

| 2022-11-21 | 82% | Bottom zone |

| 2025-10-06 | 6% | Top zone (2025 ATH) |

| 2026-04-14 | 34.4% | Current (early bear) |

As a composite, Bottom Proximity inherits the failure modes of its components. During June 2022 it read 54% — "approaching" but not "bottom zone" — which correctly flagged that confluence wasn't complete. A naive reader could still over-interpret the number.

Mitigation: Bottom Proximity > 65% is the minimum threshold to treat as "approaching bottom." > 80% is required for "in bottom zone." Below 50% is mid-cycle — no bottom call.

Historical forward-return read

The Macro historical-outcomes panel bins prior Bottom Proximity readings and reports what BTC did 7d / 30d / 90d later. Treat those medians as base rates for the current score range, not as a price forecast.

| Zone | Reading | Score |

|---|---|---|

| Deep bull / top zone | 0–15% | −2 |

| Bull / late bull | 15–35% | −1 |

| Neutral / mid-cycle | 35–50% | 0 |

| Accumulation approaching | 50–65% | +1 |

| Bottom zone | 65–80% | +1 |

| Max capitulation confluence | 80–100% | +2 |

Drawdown From ATH L2

How far below the 2-year ATH price currently sits. Deeper drawdowns historically precede higher forward returns — not because drawdown itself is bullish, but because it's a cleanest-possible proxy for cycle washout depth.

The simplest possible cycle position metric. Deeper drawdowns historically correlate with higher forward returns — not because drawdown itself is bullish, but because it's the cleanest proxy for "how washed out is the market." Every cycle bottom since 2015 had a drawdown > 70%. Every mid-cycle correction was < 55%.

We use a 2-year trailing high as the ATH anchor to avoid "fake drawdowns" during long bear markets where an old ATH is no longer the relevant reference. This aligns with how most traders think about drawdown intuitively.

| Cycle | Peak → Trough | Drawdown |

|---|---|---|

| Cycle 1 (2011-13) | $32 → $2 | −94% |

| Cycle 2 (2013-15) | $1,163 → $171 | −85% |

| Cycle 3 (2017-18) | $19,500 → $3,194 | −84% |

| Cycle 4 (2021-22) | $69,000 → $15,479 | −77% |

| Cycle 5 (2025-26) | $124,714 → $74,339 | −40% (current, in progress) |

Mid-cycle corrections can hit −30% to −55% without being cycle bottoms. 2021 had a −55% drawdown in May 2021 that fooled many into thinking the cycle was over — then BTC rallied to $69K in November.

Mitigation: Drawdown is scored +2 only at > 70%. Mid-cycle corrections never hit that threshold. The scoring band is deliberately asymmetric (−1 max near ATH, +2 max at deep drawdown) because shallow drawdowns aren't automatically bearish but deep ones are structurally bullish.

| Depth | Reading | Score |

|---|---|---|

| Near highs | 0–25% below ATH | −1 |

| Normal pullback | 25–40% below | 0 |

| Deep correction | 40–55% below | +1 |

| Bear market | 55–70% below | +1 |

| Cycle washout | > 70% below | +2 |

L3 · On-Chain Stress

Zero-FP Tier 1 Confluence L3

The "zero false positive" Tier 1 framework — four indicators that have never fired together outside of the 2015, 2018, and 2022 cycle bottoms: MVRV < 1.0, NUPL < 0, Puell Multiple < 0.5, Supply-in-Profit < 50%. The triggered count is how many of the four are currently firing.

The four indicators (MVRV < 1, NUPL < 0, Puell Multiple < 0.5, Supply in Profit < 50%) were selected by exhaustive backtesting: which combination of on-chain signals, when all firing simultaneously, has historically only occurred at cycle bottoms? These four passed the test. Individual triggers happen during corrections; all four simultaneously has only happened at the deepest cycle lows.

"Zero false positive" refers to the all-four-simultaneously confluence requirement. Partial triggers (1-3 of 4) happen throughout mid-cycle corrections and mean nothing by themselves. The framework's entire value proposition is the requirement that confluence be complete before acting.

| Date | Count | What it meant |

|---|---|---|

| 2015-01-14 | 4/4 | Cycle 2 bottom — exact |

| 2018-12-15 | 4/4 | Cycle 3 bottom — exact |

| 2022-06-18 | 1/4 | False signal — only MVRV fired, framework said WAIT |

| 2022-11-21 | 4/4 | Cycle 4 bottom — exact |

| 2026-04-14 | 0/4 | Current — no bottom confluence yet |

June 2022 had MVRV briefly cross below 1.0 during the LUNA/3AC cascade at ~$18,500. That was 1/4 Tier 1 — the framework correctly flagged it as "not confluence, wait." Price fell another 19% to $15,476 over the next 5 months before the real 4/4 bottom in November.

Mitigation: the confluence requirement is the mitigation. Never deploy maximum allocation on 1-2 Tier 1 signals. Historically the jump from 2/4 to 4/4 has taken 2-6 weeks — size up gradually as signals trigger, not all at once.

| Count | Reading | Score |

|---|---|---|

| 0 triggered | No stress | −1 |

| 1 triggered | Early stress | 0 |

| 2 triggered | Approaching bottom | +1 |

| 3 triggered | Bottom zone | +2 |

| 4 triggered | Full cycle bottom confluence | +2 |

In June 2022, all four triggered briefly during the LUNA/3AC cascade at ~$18.5K — then BTC fell another 19% into the FTX collapse at $15,476. Tier 1 confluence is necessary but not sufficient for the final low. The dashboard surfaces this warning inline on the Tier 1 panel.

LTH MVRV L3

market/mvrv_more_155Market Value / Realized Value for coins held more than 155 days — the long-term holder cohort. Because LTHs bought at much lower prices on average, LTH MVRV is typically well above 1.0 even in neutral regimes. When LTH MVRV drops below 1.0, it means the average long-term holder is underwater — historically only at the deepest capitulation lows.

Long-term holders (coins held > 155 days) are the patient cohort. They rarely spend unless forced. LTH MVRV below 1.0 means even patient holders are underwater on average — historically this has only happened at the deepest capitulation lows. It's the single strongest individual on-chain signal in the framework.

The 155-day threshold comes from long-term-holder research and was formalized in the Cointime Economics framework. See §14 cohort convention for the full derivation.

| Date | LTH MVRV | Meaning |

|---|---|---|

| 2015-01 | 0.55 | Deep capitulation — all LTHs underwater |

| 2018-12 | 0.82 | Cycle low — most LTHs near breakeven |

| 2021-11 | 6.5 | Cycle top — LTHs at peak profits |

| 2022-11 | 0.82 | Cycle low — confirmed |

| 2025-10 | 3.2 | Cycle top — still strong cohort profits |

| 2026-04 | 1.642 | Current — LTHs still +64% in profit |

LTH MVRV can be slow to reflect late-cycle changes — the cohort composition shifts slowly because new LTHs are constantly being created as STH coins age past 155 days. A freshly-minted LTH cohort entering the 155-day threshold at high prices can dilute the reading upward.

Mitigation: read LTH MVRV alongside Liveliness. If LTH MVRV is falling AND Liveliness is falling, LTHs are genuinely hoarding. If LTH MVRV is falling but Liveliness is rising, the drop is from new-LTH dilution, not real stress.

| Zone | LTH MVRV | Score |

|---|---|---|

| Full capitulation (LTHs underwater) | < 0.85 | +2 |

| LTH stress | 0.85 – 1.00 | +1 |

| Normal / accumulation | 1.00 – 2.00 | 0 |

| Late bull distribution | > 2.00 | −2 |

STH MVRV L3

market/mvrv_less_155Market Value / Realized Value for coins held less than 155 days — the short-term holder cohort. STHs bought at much more recent prices, so their MVRV swings faster than LTH MVRV. STH MVRV below 1.0 means recent buyers are underwater on average — a classic late-bear-or-correction signal.

Short-term holders (coins held < 155 days) are the reactive cohort. They bought recently, usually during the late stages of a bull market. STH MVRV tracks how underwater or profitable they are on average. STH MVRV < 1.0 happens during every sharp drawdown — not just cycle bottoms — making it a faster-reacting but weaker-confluence signal than LTH MVRV.

We keep it in the framework because it's the single best early-warning signal for "new buyer stress." When STH MVRV drops below 1 for more than 14 days, a local bottom is typically within 4-8 weeks.

| Date | STH MVRV | Outcome |

|---|---|---|

| 2018-06 | 0.91 | Mid-bear, still 6 months from bottom |

| 2018-12 | 0.68 | Cycle low |

| 2021-07 | 0.94 | Mid-cycle capitulation, led to +120% rally |

| 2022-11 | 0.75 | Cycle low (with LTH MVRV) |

| 2025-10 | 1.28 | Cycle top |

| 2026-04 | 0.918 | Current — STHs −8% underwater |

STH MVRV below 1 is too common to use as a confluence trigger alone. It fires during 30%+ corrections even in the middle of bull markets. Treating it as a buy signal in isolation produces many premature entries.

Mitigation: use STH MVRV as Tier 2 (confirming) rather than Tier 1 (confluence). It supports the case when Tier 1 is firing, but it doesn't cause action alone.

| Zone | STH MVRV | Score |

|---|---|---|

| Capitulation | < 0.85 | +2 |

| Stress (recent buyers underwater) | 0.85 – 1.00 | +1 |

| Normal | 1.00 – 1.50 | 0 |

| Elevated | 1.50 – 2.00 | −1 |

| Euphoric | > 2.00 | −2 |

Liveliness / Vaultedness L3

Liveliness measures how "active" the total BTC supply is — the ratio of coindays destroyed to coindays created. When liveliness falls, LTHs are hoarding and vaultedness rises (coins aging on-chain). When liveliness rises, LTHs are distributing. Falling liveliness during a drawdown is one of the strongest accumulation signals on-chain.

Liveliness is a Cointime Economics metric that measures how "active" the total BTC supply is. Technically it's the ratio of coindays destroyed to coindays created. In plain English: when long-term holders move their coins, Liveliness rises. When they hoard (let coins sit dormant), Liveliness falls.

Falling Liveliness during a drawdown is one of the strongest accumulation signals available — it means the most patient cohort is not just holding but actively increasing dormancy. Rising Liveliness during a bull run is a top warning — LTHs are distributing.

| Date | Liveliness | Direction |

|---|---|---|

| 2018-12 | 0.58 | Falling — peak hoarding at bottom |

| 2021-04 | 0.73 | Rising — first top warning |

| 2021-11 | 0.79 | Peak — cycle top |

| 2022-11 | 0.56 | Falling — hoarding peak at bottom |

| 2025-10 | 0.71 | Rising — distribution at top |

| 2026-04 | 0.637 | Neutral/falling (36% vaulted) |

Liveliness moves slowly. Changes of 0.02-0.03 per month are normal. It's more useful as a confirmation signal than a trigger. By the time Liveliness has clearly shifted, price has usually moved already.

Mitigation: use Liveliness as a sanity check on other signals. If LTH MVRV is dropping (suggesting accumulation) but Liveliness is rising (suggesting distribution), the two contradict and neither should be acted on.

| Condition | Liveliness | Score |

|---|---|---|

| Deep hoarding | < 0.55 | +2 |

| LTH accumulation | 0.55 – 0.62 | +1 |

| Neutral | 0.62 – 0.70 | 0 |

| LTH distribution starting | 0.70 – 0.78 | −1 |

| Heavy distribution | > 0.78 | −2 |

Realized Loss L3

indicators/realized_loss (USD/day)Daily realized loss in USD — the dollar amount of BTC moving at a loss on-chain. Sustained readings under $25M/day are the capitulation-exhaustion signal: sellers are done, the bid has absorbed the panic. Readings >$1.5B/day are active panic.

Realized Loss measures dollars moving at a loss on-chain each day. It's the capitulation meter. At cycle bottoms, daily realized loss drops to historic lows — not because no one is selling, but because everyone who was going to panic-sell has already done so. The exhaustion reading is the signal.

The < $25M/day threshold was derived from the 2015, 2018, and 2022 cycle bottoms — all three had sustained realized loss below this level in the final weeks before price reversed. Conversely, > $1.5B/day indicates active panic, usually mid-capitulation rather than end.

| Date | Realized Loss | State |

|---|---|---|

| 2015-01 | $8M/day | Exhausted — cycle bottom |

| 2018-12 | $18M/day | Exhausted — cycle bottom |

| 2020-03 | $2.1B/day | Active panic (COVID crash peak) |

| 2022-06 | $1.2B/day | LUNA cascade — peak panic, not yet bottom |

| 2022-11 | $22M/day | Exhausted — cycle bottom |

| 2026-04 | ~$180M/day | Normal (current) |

Exhaustion is a necessary but not sufficient condition. The 2019 Q2-Q3 period had sustained low realized loss but BTC then dropped another 45% into December. Realized loss exhaustion can happen multiple times during a long bear market.

Mitigation: only score +2 when combined with > 55% drawdown and at least 1 Tier 1 trigger. Exhaustion in isolation is a 0 score.

| Regime | USD/day | Score |

|---|---|---|

| Capitulation exhausted | < $25M | +2 |

| Calm | $25M – $100M | +1 |

| Normal | $100M – $500M | 0 |

| Stress | $500M – $1.5B | −1 |

| Active panic | > $1.5B | −2 |

US Spot Premium L3

Live spread between a US institutional spot quote and an offshore/global spot quote. Sustained positive premium means US institutions are aggressively bidding — one of the cleanest institutional demand signals. Sustained negative premium means offshore / retail is dominating flow.

A US institutional spot venue and offshore/global venues serve different flow cohorts. The price spread between them is the cleanest proxy for US institutional demand versus offshore/retail flow. Sustained positive premium means institutions are aggressively bidding. Sustained negative premium means offshore is dominant and institutions are disengaged or selling.

Post-ETF approval (January 2024), this signal became weaker because IBIT and other ETFs now account for much of US institutional demand — bypassing direct spot-venue flow. We still track it but weight it less than pre-2024 cycles.

| Date | CB Premium | Context |

|---|---|---|

| 2020-12 | +0.45% | Peak institutional buying — 2021 bull lift-off |

| 2021-11 | −0.28% | Distribution at cycle top |

| 2022-11 | +0.12% | Institutions bidding the low |

| 2024-01 | +0.18% | ETF launch week — sustained institutional bid |

| 2025-10 | −0.18% | Institutional distribution at top |

| 2026-04 | −0.007% | Current — neutral, just flipped slightly negative |

Post-ETF, US institutional demand routes through spot ETFs (IBIT, FBTC) which settle off-exchange. US Spot Premium no longer captures the full institutional signal. In 2024 we saw strong ETF inflows without corresponding US spot premium — the old relationship broke.

Mitigation: read US Spot Premium alongside IBIT Activity Multiplier. When both agree, institutional flow is confirmed. When they disagree, IBIT is now the more reliable signal.

| Condition | Premium | Score |

|---|---|---|

| Sustained institutional buying | > +0.10% | +2 |

| Mild premium | +0.02% to +0.10% | +1 |

| Neutral | −0.02% to +0.02% | 0 |

| Mild discount | −0.10% to −0.02% | −1 |

| Offshore-dominated flow | < −0.10% | −2 |

IBIT Activity Multiplier L3

iShares Bitcoin Trust (IBIT) is the world's largest spot BTC ETF and the cleanest proxy for US institutional spot demand. The multiplier is today's volume divided by the 30-day average. Surges (>2x) happen at both panic bottoms and FOMO tops — context matters.

IBIT (iShares Bitcoin Trust) is the largest US spot BTC ETF, typically the top 1-2 in daily volume. Post-January 2024 it became the cleanest single proxy for US institutional spot demand — surpassing the information content of US spot premium.

The "activity multiplier" is today's IBIT volume divided by the 30-day SMA. A reading of 2.0× means volume is twice normal — either FOMO buying (tops) or panic selling (bottoms). The metric is directionally ambiguous alone; it requires L2 context to interpret.

| Date | Multiplier | Context |

|---|---|---|

| 2024-01-11 | N/A | ETF launch day — no 30d history yet |

| 2024-03 | 2.4× | First ATH breakout — FOMO surge |

| 2024-08 | 0.6× | Mid-cycle lull |

| 2025-10-06 | 3.1× | Cycle top — peak FOMO volume |

| 2026-04 | 1.09× | Current — slightly elevated |

Activity surges happen at BOTH tops (FOMO) and bottoms (panic buying). Without L2 context, the signal is directionally meaningless. In 2025-10 the 3.1× surge was a clear top signal; in a hypothetical future 2026-Q4 a 3.1× surge during capitulation would be a bottom signal.

Mitigation: scored asymmetrically (−1 max, +2 max) and only read in combination with L2 halving regime. Bullish interpretation requires the surge to coincide with bear/accumulation phase.